Photo via Fast Company

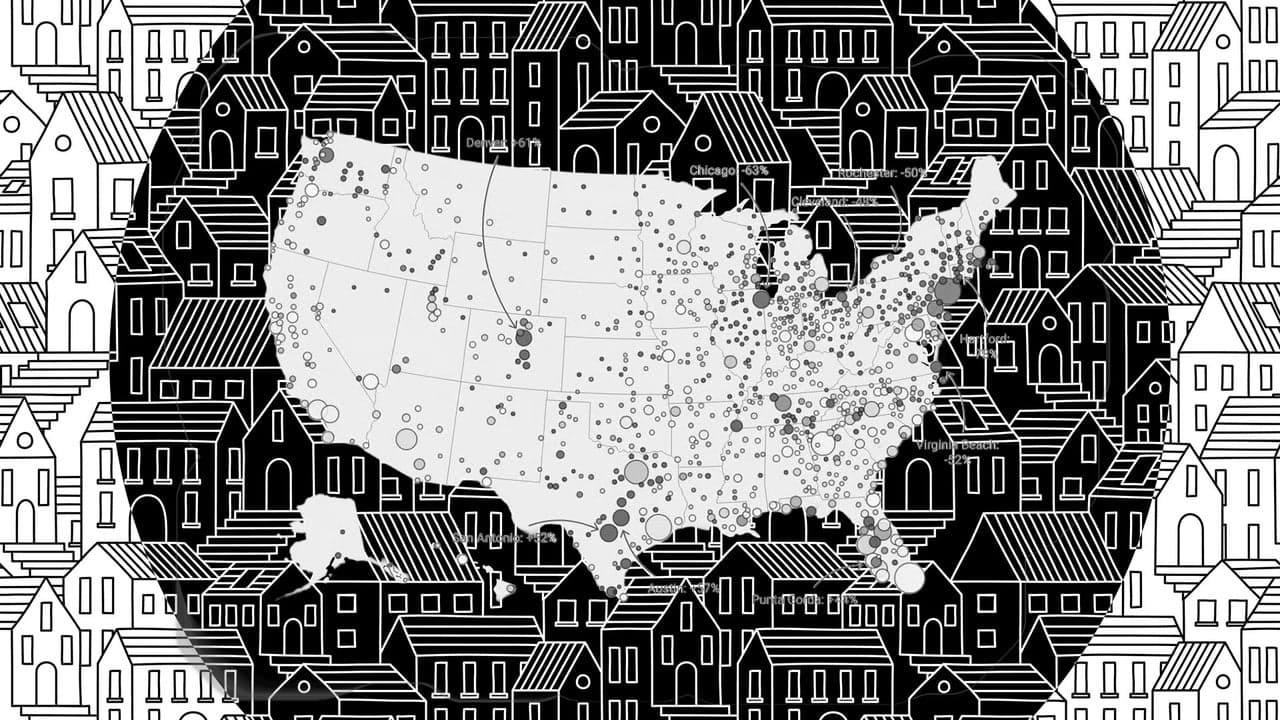

The U.S. housing market is splitting into two distinct regional camps as summer 2026 approaches, according to analysis from ResiClub. While many Sunbelt markets—including pandemic boom destinations like Austin and Punta Gorda, Florida—are experiencing home price corrections and increased buyer leverage, Northeast and Midwest markets are holding firm with constrained inventory and continued appreciation. This divergence reflects how differently regions recovered from the pandemic housing boom and subsequent market cooling.

The softening in Sunbelt markets stems from oversupply and unsustainable pricing. During the pandemic, migration-driven demand pushed home prices in Florida and Texas far beyond what local incomes could support. When domestic migration patterns normalized and mortgage rates climbed, builders responded by offering aggressive incentives and price reductions on new construction. This abundance of new supply has cooled both the new-home and resale markets, giving buyers meaningful negotiating power in these once-hot regions.

By contrast, Northeast and Midwest markets like Chicago and Milwaukee experienced minimal pandemic migration influx and have significantly less new-home construction in the pipeline. Consequently, active inventory in these regions remains 63 percent to 78 percent below pre-pandemic 2019 levels—a critical metric indicating supply constraints. Markets like Milwaukee and Hartford, Connecticut, are still recording year-over-year home price gains of 5 percent or more, demonstrating how tight inventory supports price resilience even in an otherwise cooling national market.

Atlanta-area business leaders monitoring real estate trends should note that this regional divergence has broader economic implications. Markets with sustained price growth and tight inventory often maintain stronger construction activity and related economic momentum, while correction-prone regions face headwinds in housing-dependent sectors. Understanding which regional dynamics your business serves—or might expand into—becomes critical for companies in construction, finance, retail, and workforce planning.